Kitsilano, City of Vancouver West

New real estate numbers for British Columbia’s Lower Mainland suggest that the long rise in house prices is accelerating in the City of Vancouver and adjacent suburbs.

In all these areas, the benchmark price for a detached home has surpassed a million dollars. This is far beyond the reach of most working families, with troubling side effects.

People who hold jobs in Vancouver are moving to high-priced compromise locations in the mid-suburbs to find space, or to suburban margins beyond the effective reach of public transit. They will endure long automobile-bound commutes; they’ll be detached from their new communities; even with their move away from the city, many will continue to struggle with big mortgages; and their detachment combined with their financial struggle will feed the growing general reluctance to pay for the expansion, or even the maintenance of public services.

The fast-rising price of houses in Vancouver is firmly linked in the media to an inflow of investment from China. Observers such as a former Canadian ambassador have called for the setting up of tax barriers as well as policies to shield low-income residents from eviction. However, while some local protection of rental properties is already in place, Canadian governments are not likely to take action to intervene in the home sale market, based on the following considerations.

Real estate sales are a major driver of the B.C. economy. In the 2015 provincial government budget, “real estate, rentals and leases” is shown as the largest single element in our gross domestic product, at 17.5 per cent. An inflow of foreign real estate money benefits numerous individuals who are selling properties, allowing them to purchase retirement homes or invest in new ventures. And it boosts the home equity of many homeowners, giving them additional borrowing leverage. On a separate point, many B.C. homeowners (including me) own foreign property in places like California or Arizona, and are likely to see the imposition of property purchase restrictions by Canada as a dangerous step. Finally, even a stiff tax on foreign real estate investment in Canada seems unlikely to deter the Asian multi-millionaires who are currently purchasing Vancouver real estate with cash down, sight unseen.

Real estate sales are a major driver of the B.C. economy. In the 2015 provincial government budget, “real estate, rentals and leases” is shown as the largest single element in our gross domestic product, at 17.5 per cent. An inflow of foreign real estate money benefits numerous individuals who are selling properties, allowing them to purchase retirement homes or invest in new ventures. And it boosts the home equity of many homeowners, giving them additional borrowing leverage. On a separate point, many B.C. homeowners (including me) own foreign property in places like California or Arizona, and are likely to see the imposition of property purchase restrictions by Canada as a dangerous step. Finally, even a stiff tax on foreign real estate investment in Canada seems unlikely to deter the Asian multi-millionaires who are currently purchasing Vancouver real estate with cash down, sight unseen.

To sum up in political terms, the benefits to sellers and homeowners from high housing prices are well defined. The negative effects on potential buyers, or hypothetical buyers, are more diffuse. As far as I know, nobody at the provincial or federal government levels has even offered to review the issue.

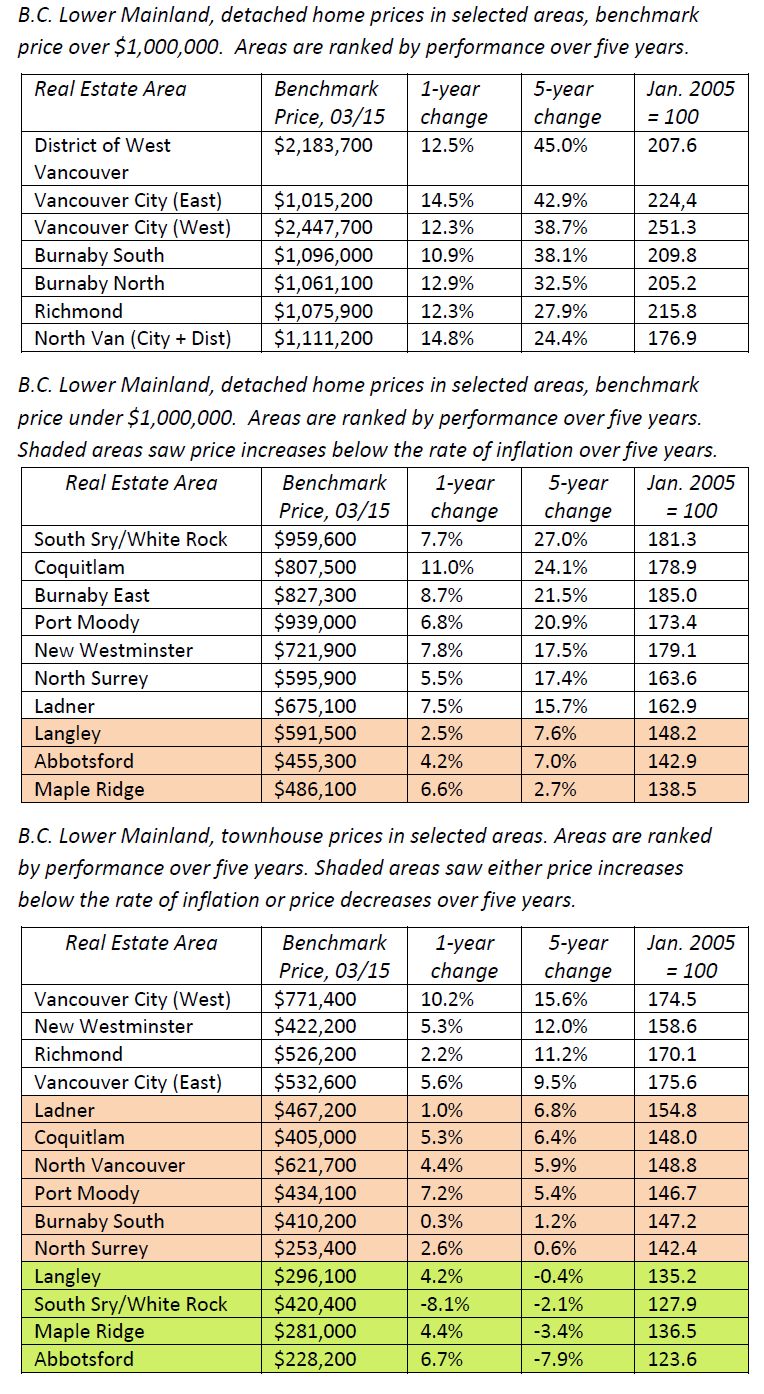

Returning to the current numbers, it’s evident that detached home prices are rising at an accelerating rate in Vancouver and nearby suburbs. The short-term trends for townhouses and apartments are patchy, but with detached homes in the upper-tier suburbs, the signal seems clear: a one-year price rise of more than 10 per cent in every area, well above recent year-over-year averages. Price ripples appear to extend across the Lower Mainland region, with significant recent price increases even in normally slow areas.

In organizing the tables below, I have emphasized the five-year horizon. For detached homes, the million-dollar suburbs are grouped together with price increases of 25 to 45 per cent over the past five years. Further out, in New West, Coquitlam and North Surrey, increases were between 15 and 25 per cent; and at the suburban margin, detached homes dropped in real value over five years.

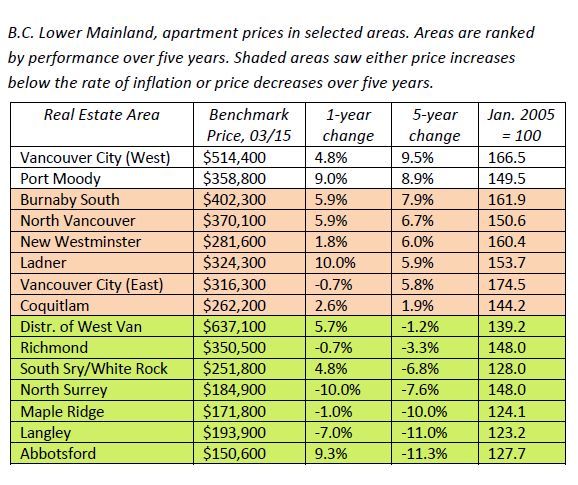

South Surrey is an anomaly, with relatively high and fast-rising house prices, despite its distance from downtown Vancouver. Apartment prices in the same area, partly due to a large stock of older apartments, are low and deteriorating.

The Lower Mainland townhouse and apartment markets are very different from the detached home market. Over five years, townhome prices have risen by less than the rate of inflation outside of Vancouver, Richmond, and New West, or else they have dropped. In the same period, apartment prices have increased by less than 10 per cent in every case, and they have dropped in many places.

The Lower Mainland townhouse and apartment markets are very different from the detached home market. Over five years, townhome prices have risen by less than the rate of inflation outside of Vancouver, Richmond, and New West, or else they have dropped. In the same period, apartment prices have increased by less than 10 per cent in every case, and they have dropped in many places.

The tables below are derived from monthly reports published by the Greater Vancouver Real Estate Board and the Fraser Valley Real Estate Board. The inflation calculation is from the Bank of Canada.

And a clarification, added 24 hours after I first posted this piece: as a townhouse owner in Maple Ridge, I am not eligible to ride the real estate gravy train. The assessed value of our home has been about static for more than five years.